in the World of Online Casinos")

")

")

Thousands of people think of purchasing their own homes at the very beginning of adult life. Buying accommodation requires getting a decent amount of money out of your pocket.

That is why most individuals postpone such an essential step. However, a great tool exists to help students become homeowners – mortgage.

Students’ mortgage programs give students a hand if they want to live in their apartment or house. Many students consider this procedure complicated because of student loans and the frequent use of payday loan apps that don’t require much time.

Nevertheless, don’t stop dreaming about your square meters just because you’re a student. All is possible! Let’s go deeper and learn more about mortgage programs for students!

Top Students’ Mortgage Programs

#1 HUD

The U.S. Department of Housing and Urban Development (HUD) simplifies purchasing a home. The program, established in 1965, is responsible for developing solid communities with affordable housing.

In this way, government agencies increase the affordability of homeownership opportunities.

If you are a novice homebuyer, HUD is one of the most intelligent decisions you can make because it has special programs for someone like you.

Moreover, it offers buyers of real estate government programs for anyone interested in buying a home.

#2 FHA

The Federal Housing Administration (FHA) provides mortgage insurance for loans from particular lenders approved by the FHA under the HUD. Due to the state guarantee, these lenders can make FHA housing loans with smaller down payments.

In contrast to traditional mortgages, students can get a loan with as low as 3.5% of the purchase price to put on deposit.

It depends on the state from which you wish to purchase. Another benefit is that the FHA mortgage gives you a lower interest rate.

The majority of those mortgages have a fixed interest rate. It is a big plus because this aspect allows virtually all population category funds up to 96.5% of the property’s purchase price. In addition, this cuts back supplemental expenses such as closing costs and assists in reducing your mortgage payments.

The impact of student loans on getting a mortgage is undoubtedly significant. Fortunately, student mortgage programs are set up to help homebuyers pay off their student loans.

#3 SmartBuy 3.0 in Maryland

If you are a resident of Maryland, you are eligible to get a mortgage program SmartBuy 3.0.

As an advantage, it provides citizens with the opportunity to purchase a home and pay off student loan debt at the same time.

Maryland SmartBuy 3.0 offers up to 15% of the buying price of the home to the borrower to repay their student debt with a payoff limit of $50,000.

#4 Student Loan Assistance Grant in Newburgh Heights, Ohio

If you want to pay off your student loan debt and acquire a home in Newburgh Heights, Ohio, this program is for you.

With the student loan assistance grant, you could qualify for a 50% grant on your student loan, up to $50,000.

Only if all program requirements are satisfied, after ten years of living in a qualifying home bought in Newburgh Heights, beneficiaries receive 80% of their award amount.

It’s important to know that one of the requirements is to buy a home for no less than $50,000.

Receiving Students’ Mortgage: Step-by-Step Guide

If you are a student who wants to achieve your goal of buying your accommodation, it’s a necessity to have a clear idea of how a mortgage works and what you need to do to receive it.

You have to grasp that getting a mortgage is an important step that demands a particular plan of specific.

Therefore, here presented a guide created to make a coherent picture of what you should do.

- Investigate the requirements established by your local bank. It’s the first and probably one of the main points you must undoubtedly pay attention to.

- Make sure, if you want it. Before making such a significant decision, ask yourself whether you are ready to have your apartment.

- Develop a plan to make your DTI better. Lenders will look at your debt-to-income (DTI) ratio when you turn to them in case of receiving a mortgage. Typically, a DTI of 43% or lower is considered good.

DTI = monthly debt payments split of your gross monthly revenue.

DTI helps this person to measure how well you can make your monthly payments and pay off your mortgage.

If you want to improve your DTI, you can find a second income or increase your hours of present work.

The lower your DTI – the better it is for your situation. If your DTI is high because of student loan payments, determine whether your payments are properly accounted for or calculated.

- Boost your credit score and set aside an advance deposit. The majority of lenders will require a down payment. This is the reason why you need to think of saving some amount of money.

Keep in mind that essential steps always include hard work. Consequently, you will pass all stages if you genuinely want to become a homeowner in student time. You should be pretty creditworthy to purchase a home with the help of a mortgage.

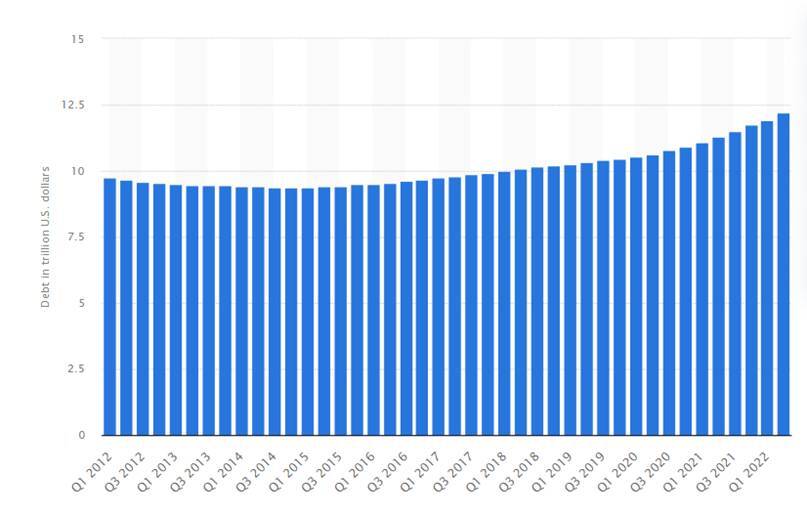

According to the table below, you can notice that the home mortgage debt of households and nonprofit organizations amounted to nearly $12 trillion in Q2 2022.

In recent years, mortgage values have been rising quickly. The minor strict controls led to the rate of home mortgage sector debt rising.

Home mortgage debt of households and nonprofit organizations in the United States from 1st quarter 2012 to 2nd quarter 2022

Does Student Loan Effect Getting a Mortgage

Every lender will have their view about student loans. Firstly, your month-to-month student loans are recorded under the debt component of DTI.

- FHA loans: The student loan’s actual monthly payment to your credit is part of the DTI formula, provided it is more than $0 per month. For $0, lenders will add 0.5% of your overall student loan debt to your DTI.

- Traditional loans: Borrowers enrolled in an income-tested repayment program may be eligible to receive a $0 payment, provided they have the necessary documentation. For deferred or forborne loans -1% of the student loan balance if you pay less than or equal to $0.

Summing Up

Nowadays, students have a fantastic ability to receive a mortgage program suitable for their position.

They can become young homeowners by taking some steps. If you wish to spend your life independently all the time, look closely at each student’s mortgage program and choose the most appropriate one.

Don’t forget that you are one step closer to your dream! Keep going!

TechnologyHQ is a platform about business insights, tech, 4IR, digital transformation, AI, Blockchain, Cybersecurity, and social media for businesses.

We manage social media groups with more than 200,000 members with almost 100% engagement.

in the World of Online Casinos")

{kind=link}